All Weather Portfolio 2.0

How the idea of an all-season portfolio has evolved — and why its next iteration lives on the blockchain

The Concept That Transformed Asset Management

In the late 1980s, Ray Dalio set out to solve a problem no one had approached systematically before: how to construct a portfolio for his personal trust fund that would survive any economic environment — including those he would never live to see. The framework was first articulated in 1988–1989, and in 1996 Bridgewater officially launched the All Weather fund.

Dalio’s logic rests on a straightforward observation: at any given moment, the economy occupies one of four distinct regimes — economic growth, inflation, deflation, or recession. Every asset class performs well in some environments and poorly in others. Equities thrive in growth with moderate inflation. Bonds benefit from deflation and recession. Gold and commodities excel during inflationary shocks. The portfolio manager’s task, in Dalio’s framework, is not to predict which regime comes next, but to hold roughly equal “risk bets” across all four scenarios.

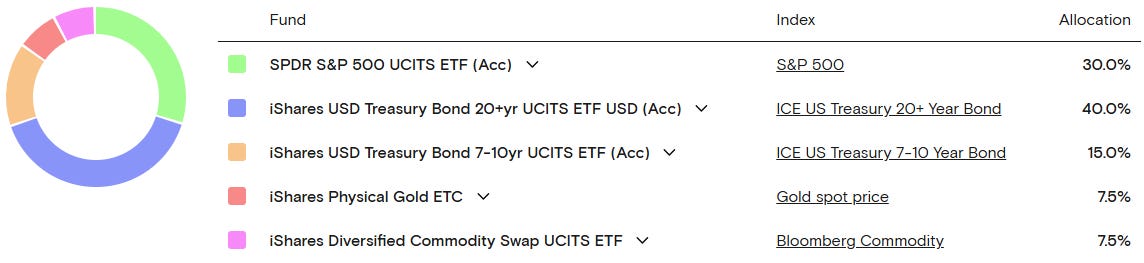

This insight gave rise to the classic All Weather allocation: 30% US equities, 40% long-term Treasuries, 15% intermediate-term Treasuries, 7.5% gold, 7.5% commodities. The disproportionately large fixed income weight is not a reflection of conservatism — it is mathematics. Bonds carry substantially lower volatility than equities, and achieving risk parity requires a larger nominal allocation to balance the contribution of each asset to overall portfolio risk.

For three decades, the portfolio performed brilliantly. Drawdowns in most crisis years remained manageable. Real returns consistently outpaced inflation. The framework appeared close to perfect.

Why the Classic All Weather Broke Down

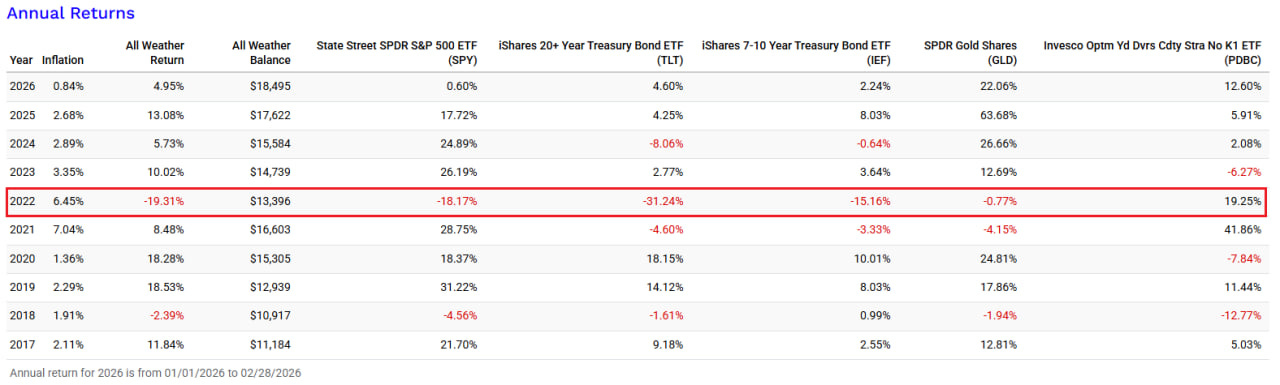

2022 was a watershed moment for portfolio managers — one that recalled the stagflationary collapse of the 1970s. The classic All Weather portfolio lost approximately 20%, a result in direct contradiction with its stated philosophy.

The failure stemmed from the simultaneous decline of both equities and bonds. Historically, these two asset classes maintained a negative or near-zero correlation: when one fell, the other held or rose. That relationship was the structural foundation of the entire framework. But in 2022, the Federal Reserve launched the most aggressive tightening cycle in forty years, responding to an inflation shock driven by pandemic-era fiscal stimulus and the breakdown of global supply chains. In an environment of rapidly rising rates, long-duration bonds suffer severe price losses. Simultaneously, higher discount rates compress equity valuations. The diversification mechanism underpinning the entire portfolio ceased to function.

Since then, the geopolitical landscape has been fundamentally restructured. Armed conflicts, trade wars, fragmentation of global capital markets, and de-dollarization are structurally altering the behavior of traditional assets. The equity-bond correlation — negative for decades — has periodically flipped positive in the new regime, and it does so precisely when protection is most needed.

Against this backdrop, we propose rethinking the all-weather framework for the current reality. But before moving to specific iterations, it is worth establishing the selection criteria for new components. An asset is useful in this context if it satisfies at least one of three conditions: low or negative correlation with existing holdings, an independent return stream uncorrelated with broad market direction, or defensive properties in specific market regimes.

By these criteria, four directions stand out:

Cryptocurrencies — and bitcoin in particular — as an emerging alternative reserve asset

Emerging market sovereign bonds with investment-grade credit ratings

DeFi lending protocols as generators of stable, market-independent yield

Delta-neutral strategies as instruments that earn regardless of market direction

We will add each component sequentially, observing how the portfolio’s risk-return profile evolves at each step.

Iteration 1. Adding Bitcoin

Bitcoin remains the most contested asset in any institutional portfolio discussion. Critics point to its elevated volatility and its periodic positive correlation with risk assets. Proponents cite scarcity, decentralization, and the ongoing institutional adoption thesis.

The reality, as usual, is more nuanced than either camp acknowledges. Bitcoin exhibits regime-dependent correlation: during broad market selloffs it frequently declines alongside equities in a risk-off environment, yet during inflationary episodes and currency crises it tends to behave as a store-of-value asset. The core argument for its inclusion is asymmetry — a bitcoin allocation modestly increases drawdowns in adverse years while materially enhancing returns over multi-year horizons.

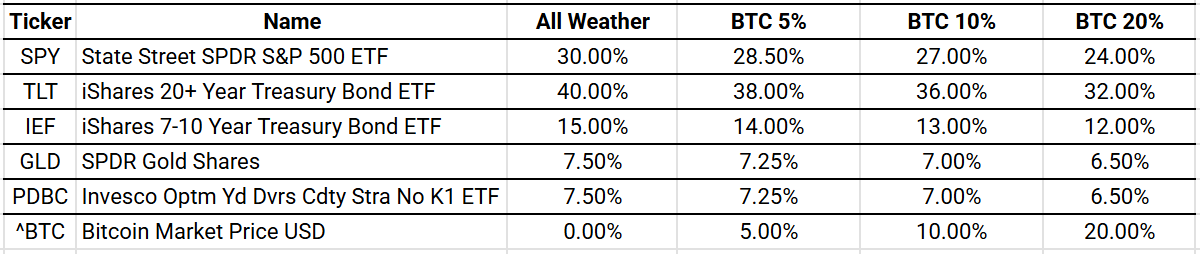

BlackRock — the world’s largest asset manager — recommends that institutional investors allocate 1–2% to bitcoin. We take that as a conservative baseline and examine more meaningful allocations — 5%, 10%, and 20% — funded proportionally by reducing equities, bonds, and other existing positions.

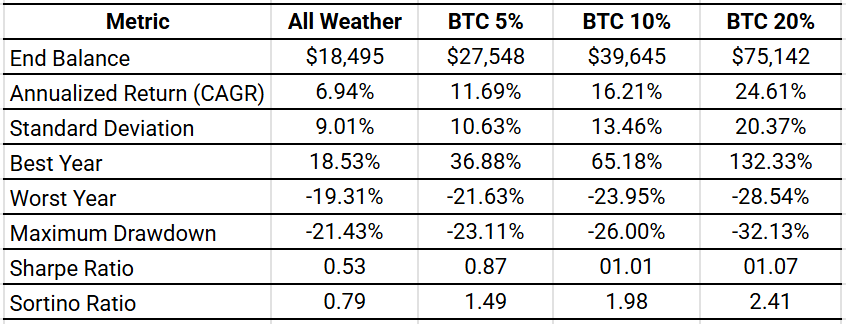

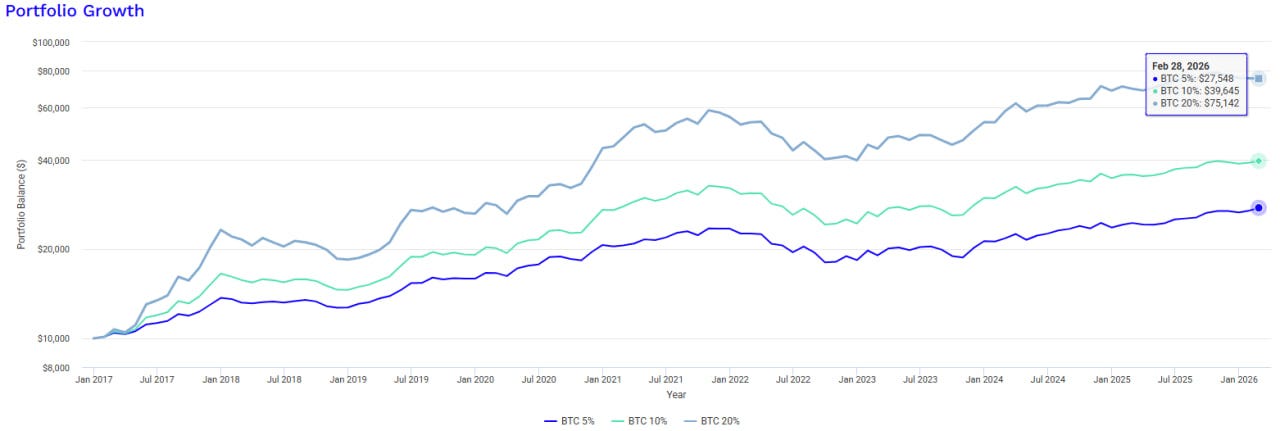

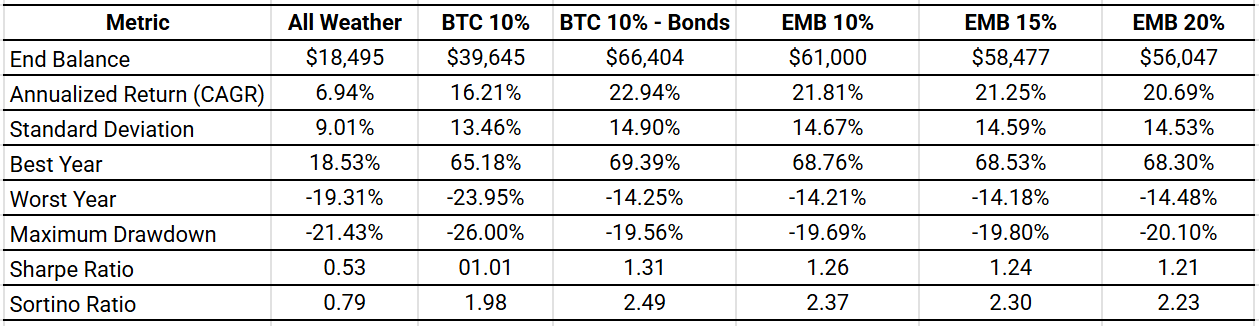

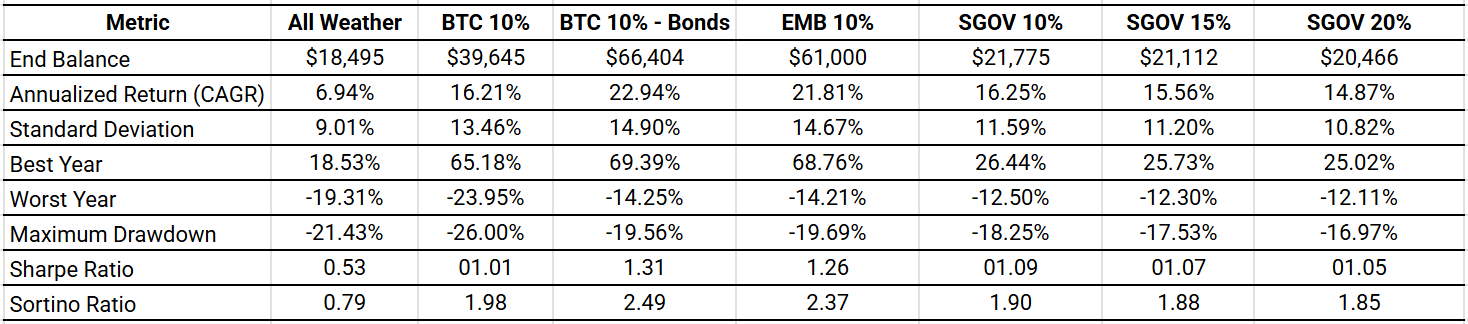

A nine-year backtest from 2017 to 2026 with a $10,000 starting capital provides a compelling picture of how bitcoin reshapes the portfolio’s profile.

Moving from the classic All Weather to a 10% BTC allocation increases CAGR from 6.94% to 16.21% — more than doubling the annualized return. Maximum drawdown deteriorates only from −21.43% to −26.00%, a difference of 4.57 percentage points. This asymmetric trade-off is precisely the case for including bitcoin in a diversified portfolio.

The Sharpe ratio of the classic All Weather stands at just 0.53 — meaning the portfolio generates less than one unit of excess return per unit of risk. At BTC 10%, it crosses the psychologically significant threshold of 1.0. The Sortino ratio — which measures return quality relative to downside volatility only — rises from 0.79 to 1.98. In effect, the portfolio with a 10% bitcoin allocation generates returns more efficiently for the same level of harmful drawdown.

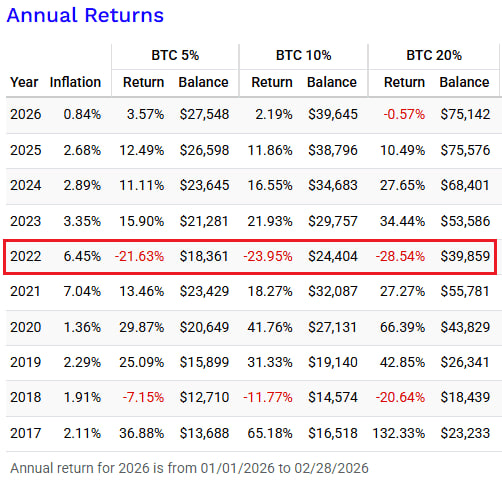

2022 is the strongest argument against bitcoin in a portfolio. The classic All Weather lost −19.31%; BTC 20% fell −28.54%. The gap is meaningful, but context matters: 2022 was a year in which virtually every asset class declined simultaneously under the most aggressive Fed tightening cycle in four decades. Even in the worst year on record for the industry, adding bitcoin worsened outcomes by less than 9 percentage points — while in favorable years, BTC 20% delivers multiples of the baseline return.

The compounding argument is the most compelling. Over nine years, $10,000 in the classic All Weather grew to $18,495. With a 10% BTC allocation, the same capital reached $39,645 — 2.1x more. At 20% BTC, it reached $75,142 — four times the starting balance.

In our view, 10% represents the optimal bitcoin allocation — the most balanced point in the risk-return space. This is where the inflection occurs: the Sharpe ratio crosses 1.0, CAGR more than doubles relative to the baseline, and the position functions as an option on global monetary transformation with a well-defined downside.

Iteration 2. What If We Remove Treasuries Entirely?

A provocative question — but a legitimate one. If bonds no longer perform their risk-balancing function with the reliability they once did, what is the rationale for holding them?

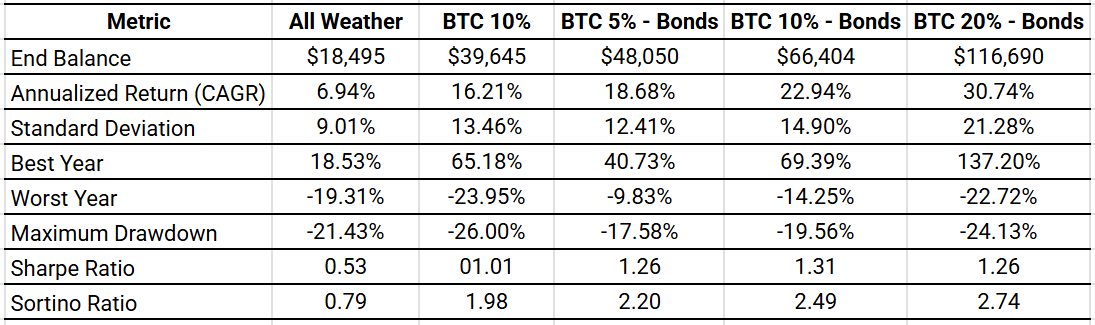

We test a four-component portfolio: equities, gold, commodities, and bitcoin. No fixed income.

Backtest results, 2017–2026:

The key finding defies conventional intuition: removing bonds did not meaningfully increase portfolio volatility. The BTC 10% bond-free portfolio shows a standard deviation of 14.90%, versus 13.46% for BTC 10% with bonds — a modest difference. But in the context of maximum drawdown, the picture is striking: −19.56% versus −26.00%. The very instruments designed to protect the portfolio were, in reality, deepening drawdowns during periods of simultaneous cross-asset pressure.

2022 provides the clearest illustration. In the year that effectively invalidated the classic All Weather (−19.31%), the bond-free portfolio with 5% BTC lost only −8.15%. The reason is straightforward: TLT and IEF — which fell −31.24% and −15.16% respectively under the Fed’s rate hike campaign — were no longer part of the portfolio.

The Sharpe ratio of the bond-free BTC 10% portfolio reaches 1.31, the highest across all tested configurations. The Sortino ratio rises to 2.49, nearly three times the classic All Weather figure.

The conclusion is counterintuitive but supported by the data: eliminating bonds did not merely preserve the risk profile — it improved it across several key metrics. Higher Sharpe, lower maximum drawdown, a more contained worst year, and materially higher returns. Commodities and gold, combined with bitcoin, provide economic regime diversification comparable to bonds — without the interest rate sensitivity that proved destructive to any long-duration fixed income holding in 2022.

In an environment of structurally elevated rates and geopolitical fragmentation, a bond-free portfolio can be simultaneously more resilient and more profitable. This observation sets up the next iteration naturally: we will bring bonds back — but a fundamentally different kind.

Iteration 3. Emerging Market Bonds

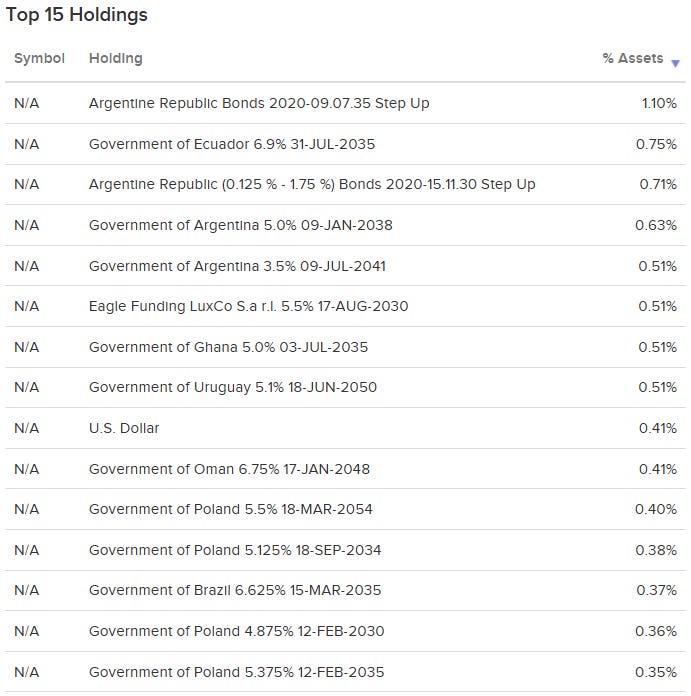

If the problem with US Treasuries is their sensitivity to Federal Reserve policy and the mounting US fiscal burden, the logical alternative is investment-grade sovereign debt from emerging markets. We are not referring to high-yield paper with default risk, but to a well-established instrument: the iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB) — one of the largest and most liquid ETFs in the segment, covering sovereign debt from more than 30 countries.

A critical distinction is currency risk. Local-currency EM bond exposure is substantial and can entirely erode returns during periods of dollar strength. EMB addresses this directly: the fund invests exclusively in hard currency debt — sovereign bonds denominated in US dollars. The investor captures a yield premium over US Treasuries without taking on currency volatility.

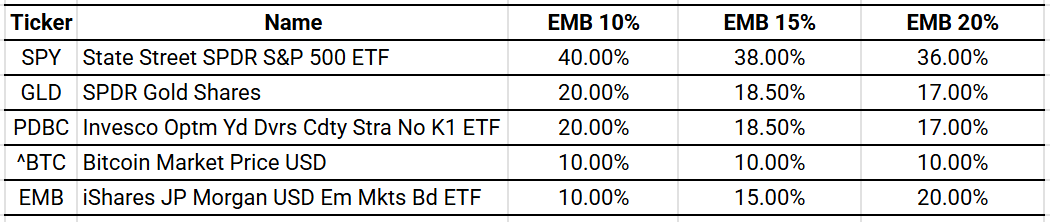

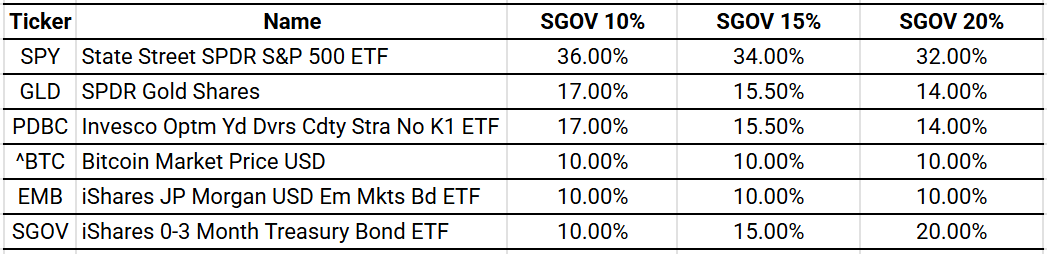

We test three configurations — EMB 10%, 15%, and 20% — with a fixed 10% bitcoin allocation and proportional reductions in remaining positions.

Backtest results, 2017–2026:

EMB 10% approaches the bond-free portfolio’s return and surpasses it on resilience. The gap between the two is $5,404 — less than 9% of the terminal balance over nine years. This is a modest cost for a measurable improvement in volatility characteristics: standard deviation falls from 14.90% to 14.67%, and the Sortino ratio holds at 2.37 versus 2.49 — a minimal difference in the quality of risk-adjusted return.

The most revealing metric is worst-year performance. EMB 15% posts the best result across the entire comparison: −14.18%. This edges out the bond-free portfolio and represents a substantial improvement over the classic All Weather (−19.31%) and BTC 10% with US Treasuries (−23.95%). Despite its reputation for risk, EM hard currency debt behaved far more predictably in 2022 than long-duration US bonds — simply because it carried far less duration sensitivity.

The law of diminishing returns applies clearly here: each additional 5% in EMB costs approximately 0.5–0.6 percentage points of CAGR, while producing only 0.1–0.2 pp of volatility improvement. Allocations beyond 10% in EMB deliver decreasing marginal benefit at a persistent return cost.

A 10% allocation to EMB restores structural all-weather properties — a coupon-generating instrument that produces income independent of equity market direction — without sacrificing the return profile built in prior iterations. This configuration forms the foundation for what follows.

Iteration 4. DeFi Lending

Decentralized lending protocols represent one of the few genuinely new return sources to emerge in recent years. Aave, Morpho, Kamino, Euler — all operate on the same fundamental mechanic: users deposit assets into a smart contract and earn interest income from borrowers who access liquidity against collateral.

From a portfolio management perspective, this is compelling for several reasons:

Yield. Stablecoin lending rates in major protocols have historically ranged from 3% to 12% annually depending on the market cycle — competitive with traditional money market instruments, with superior accessibility and liquidity

Correlation. DeFi lending yields are driven by demand for leverage within the crypto ecosystem, not by the directional movement of traditional markets. Rates rise when the crypto market overheats — meaning this return source activates precisely when other risk assets carry elevated risk

Liquidity. Capital in major protocols is redeemable at any time, without lock-up periods — an uncommon feature among alternative investments

A transparent analysis, however, requires acknowledging the limitations of this iteration. Rigorous backtesting of DeFi protocols is not possible — they have no tradeable ticker history. As a proxy, we use the iShares 0–3 Month Treasury Bond ETF (SGOV), a short-duration money market instrument with a broadly similar profile of stable, low-volatility returns. This is a conservative approximation. Real DeFi protocols have historically generated higher yields than SGOV, with no correlation to traditional markets — meaning actual portfolio outcomes would likely be more favorable than our model reflects.

Backtest results, 2017–2026:

SGOV as a proxy is, candidly, a weak representation of DeFi yield — but a valuable one for risk analysis. The terminal balance of the SGOV 10% portfolio disappoints relative to EMB 10% and the bond-free configuration. A CAGR of 16.25% is a meaningful step back from prior iterations, a direct consequence of substituting money market yields for the return premium of EM debt or bitcoin. These figures should not be read as a forecast for DeFi lending performance.

Where SGOV delivers, however, is on downside protection — the best results in the entire comparison set. SGOV 20% posts the lowest maximum drawdown and the best worst-year performance across all tested configurations. This confirms that a money market-like component systematically reduces drawdown depth. This is precisely the role DeFi lending should play in a live portfolio — at yields roughly twice those of SGOV, and without correlation to traditional market factors.

The modeling supports a 10% allocation as the appropriate anchor for money market instruments. Scaling beyond 10% delivers diminishing marginal protection at an increasing cost to total return — this holds even for real DeFi protocols. The next step is an instrument that generates returns regardless of whether markets rise or fall.

Iteration 5. Delta-Neutral Strategies

This is perhaps the least intuitive but one of the most structurally valuable components of the updated portfolio. Delta-neutral strategies generate returns not from directional market exposure, but from structural inefficiencies embedded in market microstructure — and for precisely this reason they complement the framework we have built across prior iterations.

The most accessible variant is basis trading, or cash-and-carry, in the crypto markets. The mechanic is straightforward: buy bitcoin in the spot market and simultaneously open an equivalent short position in bitcoin futures. The resulting position is fully hedged against BTC price movement — a 10% rally in spot is offset by an equal loss in the futures leg. Returns are extracted from two sources: the basis (the spread between futures price and spot price) and the perpetual funding rate.

The funding rate is the key mechanism. In perpetual futures contracts, traders holding long positions pay traders holding short positions every eight hours — or vice versa, when the market is in a downtrend. During bull markets, when demand for leveraged long exposure is elevated, longs pay shorts — and the delta-neutral position holder collects these payments as a steady cash flow stream, without assuming any directional price risk in BTC.

Historically, cash-and-carry strategies in crypto have generated annualized returns in the range of 10–15%. During periods of peak market exuberance, rates have been substantially higher — annualized funding in the most frenzied phases of bull cycles has reached 50%. During bear markets, returns compress and can turn negative as short positioning dominates and funding reverses.

No public ETF accurately replicates the parameters of basis trading — a rigorous backtest on the same basis as prior iterations is not feasible. That said, the performance record of funding rate arbitrage is well documented: according to BitMEX data covering nine years of perpetual futures history on bitcoin, the funding rate was positive in 71.4% of all periods, providing consistent positive carry for delta-neutral position holders. Real-time funding rate data across major venues is aggregated by CoinGlass.

In our view, delta-neutral strategies should not exceed 15% of the portfolio. At this sizing, the allocation functions as a return stabilizer in sideways and upward-trending markets without creating excessive concentration risk in the event of operational failures.

Scenario Matrix

Returning to Dalio’s methodology, we can now evaluate how the updated portfolio covers all four economic regimes across its full set of components.

No single component performs across all four regimes simultaneously — by definition, no such asset exists. But taken together, the five return sources ensure that at least two or three components are actively contributing in any given phase of the cycle.

The contrast with the classic All Weather is instructive. In an inflationary regime, Dalio’s original portfolio relied exclusively on gold and commodities. The updated version adds bitcoin, elevated DeFi lending rates, and enhanced delta-neutral funding as additional contributors. In a recessionary environment, the original framework leaned on long-dated Treasuries — which, as 2022 demonstrated, can fail when most needed. Here, that role is distributed across EM bonds, gold, and DeFi lending, which continues to generate cash flow independent of market direction.

Dynamic Rebalancing

All prior iterations described static allocations. But professional asset management is not a one-time distribution of capital — it is a continuous process. A professional manager does not set a portfolio and walk away; they read the market continuously and adjust exposures accordingly.

Rebalancing triggers fall into three categories:

Calendar-based — quarterly or semi-annually, weights are restored to target levels regardless of market conditions

Threshold-based — when any component drifts more than a defined percentage (e.g., 5 pp) from its target weight, rebalancing is triggered irrespective of market conditions. This mechanically enforces a buy-low, sell-high discipline without subjective market judgment

Signal-based — the most sophisticated and potentially valuable type: allocations are adjusted in response to market indicators, responding systematically to regime changes rather than attempting to predict them

The most informative signals for this portfolio are:

VIX above 30 — a systemic fear indicator. Reduce equity and BTC exposure; increase EM bond and stablecoin allocations in DeFi protocols

Negative perpetual funding rate — the crypto market has transitioned into a bearish regime. Scale down or close delta-neutral positions; reallocate to DeFi lending

EM credit spread widening — a stress signal for developing markets. Reduce EMB allocation

On-chain BTC metrics — MVRV-ratio at elevated levels historically signals overheating. Trim BTC exposure; rotate into stablecoins

It is important to draw a clear distinction: rebalancing is not market timing. We are not attempting to call tops or bottoms. We are systematically maintaining a target risk profile — harvesting gains from outperforming components and adding to underperforming ones in a rules-based, disciplined manner.

A final note on the role of cash and stablecoins in the portfolio. The 5% liquidity reserve serves three purposes: funding rebalancing operations without forcing asset sales at inopportune moments; deploying quickly when extreme dislocations create entry opportunities; and providing a survival buffer during crisis scenarios while other components recover. In an on-chain implementation, this reserve is simultaneously deployed in DeFi lending — meaning the portfolio’s “cash” earns 4–8% annually while remaining instantly accessible.

A Portfolio Without Intermediaries

This is what makes the entire construction genuinely transformative — not any individual component, but the system as a whole.

Every component described in this paper can be implemented on a public blockchain — without brokers, custodians, or asset managers issuing opaque quarterly reports. Tokenized equities and indices already trade on decentralized exchange platforms. EM bonds in fully on-chain form are currently accessible through a limited but growing set of RWA tokenization protocols. Bitcoin is native to the on-chain environment. DeFi lending and delta-neutral strategies exist exclusively in on-chain form.

For the investor, this changes four things fundamentally:

Accessibility. A traditional multi-strategy hedge fund requires a minimum investment of $500,000 or more, accredited investor status, and typically imposes a one-year lock-up period. An on-chain implementation reduces the minimum threshold to a few hundred dollars. A strategy previously available only to institutional capital becomes accessible to any investor with an internet connection.

Transparency. Every action taken by the portfolio manager is recorded on a public blockchain and verifiable by any participant in real time. Not a quarterly report with a conveniently selected benchmark — a complete, immutable transaction history auditable at any moment. This represents a fundamentally different standard of accountability relative to traditional asset management structures.

Liquidity. The portfolio operates 24 hours a day, 365 days a year. No T+2 settlement periods, no subscription windows, no market holidays. An investor in Cape Town, São Paulo, Sydney, or Helsinki accesses the same strategy at the same time under identical conditions — not a marketing claim, but a technical property of public blockchain infrastructure.

Composability. On-chain protocols function as open building blocks. A manager can combine Aave, Uniswap, GMX, and tokenized RWA into a unified strategy executed as a single smart contract — without manual reallocation between platforms and without the operational risk of human error.

Dalio’s All Weather portfolio was a revolution in its time: it systematized risk management in an era of paper trade tickets and telephone orders. Its successor is built on infrastructure that operates without interruption, is open to everyone, and requires trust in no intermediary. This is where the best ideas in traditional portfolio management meet the capabilities that have only recently become available.

Target Allocation

The path from classic All Weather to next-generation on-chain implementation can be summarized in the following target allocation:

Global Equities — 30%

Bitcoin — 10%

Gold — 10%

Commodities — 10%

EM Hard Currency Bonds — 10%

DeFi Lending — 10%

Delta-Neutral Strategies — 15%

Liquidity Reserve — 5%

This is a starting point, not a fixed prescription. Weights are adjusted based on the market cycle, investment horizon, and individual risk appetite. The portfolio lives and breathes with the market. The All Weather concept has evolved — and its next version runs on the blockchain.

If you found this research useful, we recommend our previous publications:

Money Market Instruments: From Classic Repo to Tokenized Funds in DeFi

RWA Deep Dive. A Study of the Tokenized Asset Market

Project website · Telegram channel

This material has been prepared for research and informational purposes only and does not constitute investment advice, an offer to buy or sell any financial instrument, or a solicitation of any kind. All backtest results are based on historical data and are not indicative of future performance. Investing in the instruments described in this paper involves significant risks, including but not limited to: market volatility and potential loss of capital; smart contract vulnerabilities in DeFi protocols; oracle manipulation risk; counterparty risk on centralized platforms; regulatory uncertainty across jurisdictions; on-chain liquidity risk during periods of market stress; currency risk for non-USD investors; and operational risk including irreversible loss of wallet access. Allocations to DeFi protocols should be limited to audited platforms with an established track record and substantial total value locked. Conduct your own due diligence and consult a qualified financial advisor before making any investment decisions.