Money Market Instruments: From Classic Repo to Tokenized Funds in DeFi

The repo market is one of the load‑bearing pillars of the global financial system. It is estimated at roughly $18 trillion and provides short‑term funding for banks, broker‑dealers, and hedge funds, serves as a key implementation tool for central banks monetary policy, and anchors collateral valuation across global securities markets.

Today, at the intersection of traditional finance and decentralized protocols, a fundamentally new layer of infrastructure is emerging that can reshape investor access to money market instruments. Tokenized money market funds have already surpassed $10 billion in assets under management, while the overall capitalization of tokenized real‑world assets (RWA) exceeds $25 billion. In this paper, we explore the full stack: from the mechanics of repo in developed and emerging markets to carry‑trade strategies with tokenized assets in DeFi.

Repo Mechanics

A repurchase agreement (repo) is a short‑term secured funding transaction in which one party sells securities to another with a commitment to repurchase them at a pre‑agreed price on a specified date. The difference between the sale price and the repurchase price is the repo rate, which effectively represents the interest on a collateralized loan.

A classic (or “repo”) leg is when you deliver your securities and receive cash (you borrow). A reverse repo is the opposite: you provide cash and receive securities as collateral (you lend).

For the cash provider (liquidity provider) the transaction is economically a secured loan, while for the borrower (collateral provider) it is a short‑term funding tool. In the event of the seller’s default, the buyer, as the legal owner of the collateral, has the right to liquidate it in the market to cover losses.

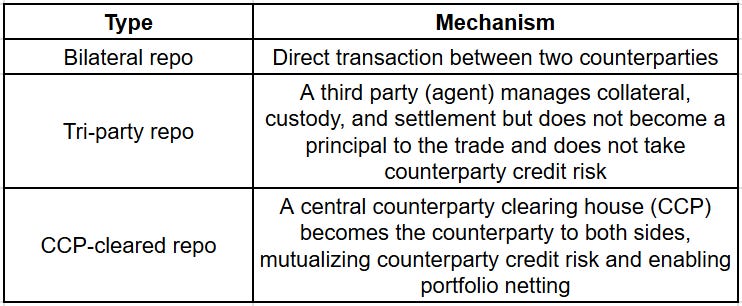

Forms of repo

Market participants

Repo market participants form an ecosystem where credit, collateral, liquidity, and interest rates intersect. Core groups include:

Dealers and banks – use repo as a primary source of short‑term funding for trading books. They run long bond inventories on balance sheet and finance them via repo, capturing the spread between bond yields and funding costs.

Money market funds (MMFs) – the largest providers of cash to the repo market, channeling liquidity from corporate treasuries and retail investors.

Hedge funds – key users of leverage in the repo market. Top funds secure minimal haircuts, enabling strategies levered 10x and higher.

Pension funds and insurance companies – deploy excess liquidity via reverse repo, earning moderate yields with minimal credit risk.

Central banks – use repo and reverse repo operations for liquidity management and to implement monetary policy.

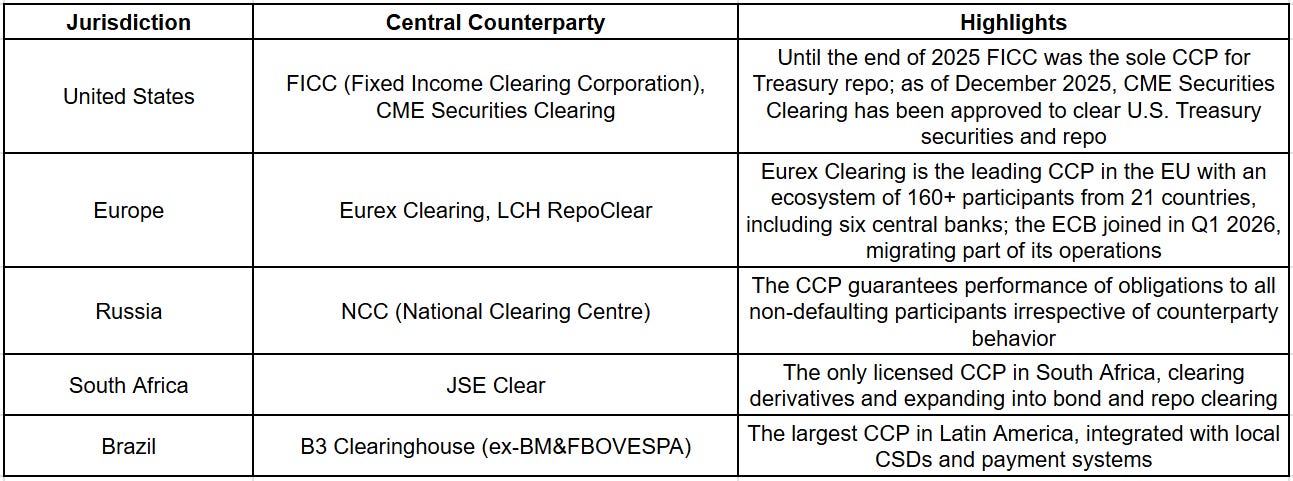

Central counterparties

The central counterparty (CCP) is a critical institutional mechanism for reducing systemic risk in the repo market. The CCP effectively “splits” the original transaction into two: it becomes the buyer to every seller and the seller to every buyer. Even if one participant defaults, the CCP ensures settlement for the non‑defaulting party.

Repo Risks

Counterparty credit risk – mitigated via CCPs but never fully eliminated, as the CCP itself can become a source of residual credit risk.

Collateral liquidity risk – surfaces under stress when collateral assets can no longer be converted to cash quickly at fair value. In March 2020, amid COVID‑19 panic, corporate bond spreads blew out while order book depth collapsed; dealers and funds were forced to sell corporate bonds at deep discounts to meet repo margin calls, amplifying fire sales and further eroding market liquidity.

Interest rate (rollover) risk – most repos are overnight and require daily roll. Once the market refuses to roll positions on previous terms, leveraged portfolios come under pressure: funding costs rise, haircuts widen, and investors are forced into rapid deleveraging.

Operational risk – particularly acute in bilateral repo without CCP intermediation.

Money Market Funds

Portfolio composition

Money market funds (MMFs) are among the most conservative forms of pooled investment, focusing on capital preservation, high liquidity, and returns in line with short‑term interest rates. A typical MMF portfolio includes:

Treasury bills (T‑Bills) – short‑term government bonds (up to 1 year in the U.S.).

Repo and reverse repo transactions – secured short‑term lending operations.

Commercial paper (CP) – unsecured short‑term corporate debt.

Certificates of deposit (CDs) – bank debt instruments with fixed tenors.

U.S. fund examples

| Fund | Ticker | AUM | Yield | Fee |

| Vanguard Federal MMF | VMFXX | ~$374 billion| ~3,58% | 0,11% |

| Fidelity Government MMF | SPAXX | ~$439 billion | ~3,83% | 0,42% |

| Fidelity Money Market | SPRXX | ~$134 billion | ~3,89% | 0,42% |

| JPMorgan Prime MMF | VMVXX | ~$100 billion | ~3,34% | 0,48% |

| Vanguard Treasury MMF | VUSXX | ~$44.5 billion | ~3,62% | 0,07% |

The Repo Pyramid

Rehypothecation (re‑use of collateral) is the fundamental mechanism through which the repo market creates leverage at the system level. When a borrower delivers securities to a lender under a repo, the lender, having obtained legal title, can re‑use them: pledge them into another repo, sell them, or onward‑deliver to a third party.

This process builds a “repo pyramid” – a chain of sequential transactions in which the same security is pledged multiple times:

Institutional investor A buys a bond for $100 and repos it out with a 2% haircut, receiving $98 in cash.

Using the $98, the investor purchases new bonds and again finances them in repo, obtaining $96.04.

The process repeats, forming a geometric progression.

With a 2% haircut, the theoretical leverage ceiling is 50:1. In other words, each dollar of equity can support a $50 bond position. The aggregate exposure created through rehypothecation can significantly exceed the amount of physically outstanding securities – a phenomenon commonly referred to as the collateral multiplier.

Real‑world scale

The most prominent manifestation of the repo pyramid is the Treasury basis trade – an arbitrage strategy where a hedge fund buys Treasuries financed via repo and simultaneously sells futures on equivalent Treasury contracts. The price difference (basis) is the profit driver, but given its small magnitude (20–45 bps), the trade is typically run with 10–20x leverage.

According to FSB estimates, hedge fund borrowing in the repo market is on the order of $3 trillion – roughly 25% of their aggregate assets. The largest 10 hedge funds obtain near‑zero haircuts, enabling them to run “substantially higher” leverage than smaller players, as highlighted by the Bank for International Settlements.

Tokenization and DeFi: New Opportunities for Investors

Barriers of traditional infrastructure

One of the structural limitations of the traditional financial system is the complexity of cross‑border access to investment products. For an investor from South Africa or India to allocate to Brazilian securities markets or, say, purchase units of a money market fund in another jurisdiction, they typically must:

Open a brokerage account in the relevant jurisdiction and pass KYC/AML.

Manage double taxation issues.

Overcome logistical, infrastructural, and regulatory hurdles.

Local currency volatility adds yet another layer of risk. For retail and mid‑sized institutional investors, such cross‑border strategies are often economically inefficient. On top of that, a $3,000 minimum for a Vanguard money market fund is already a high entry threshold, not to mention various vehicles with minimum tickets of $50–100–150 thousand.

Current landscape of TMMFs

Tokenization fundamentally changes this paradigm. Tokenized money market funds (TMMFs) map each digital token to a pro‑rata share in the underlying fund; smart contracts govern subscriptions, redemptions, and transfers, ensuring operational efficiency and regulatory compliance.

Key products in the market include:

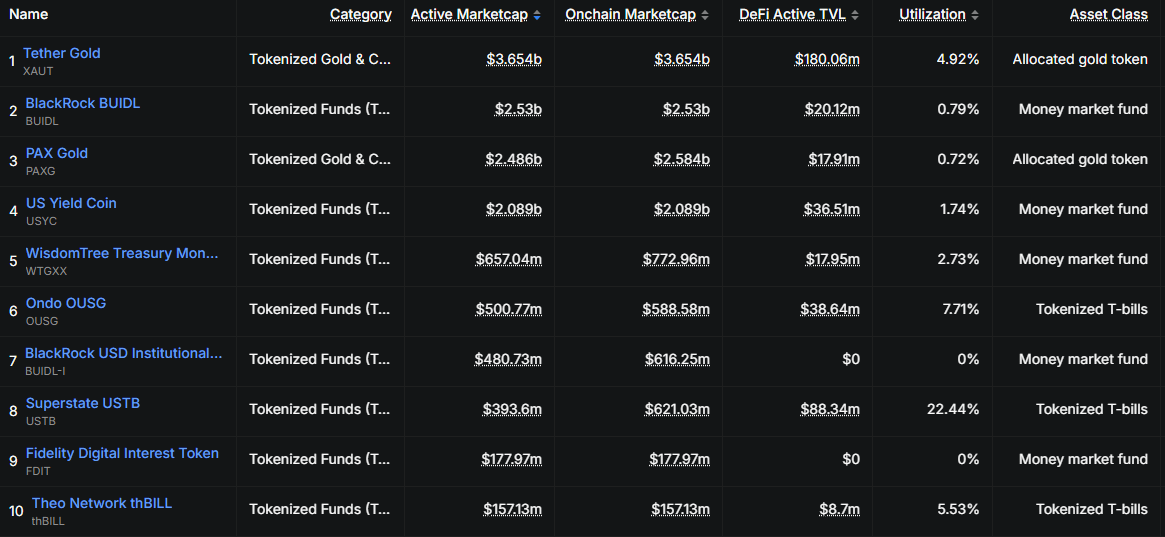

| Product | Issuer | AUM |

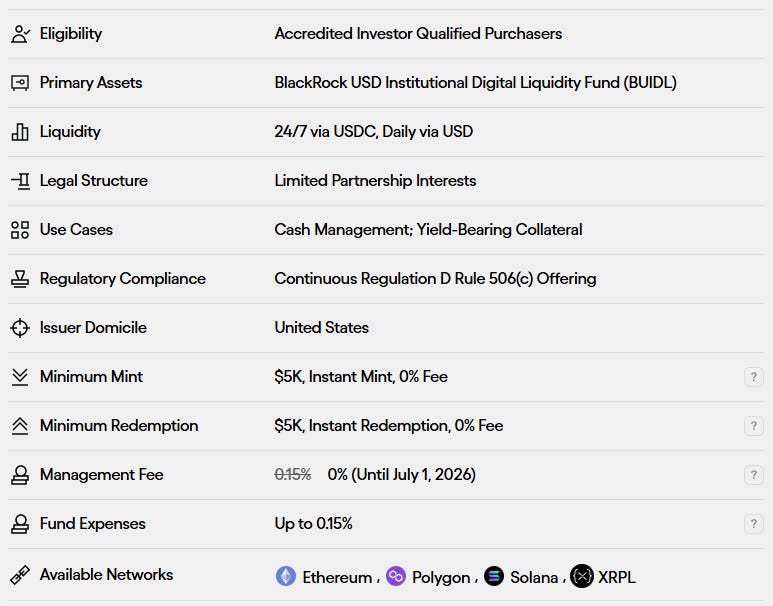

| BUIDL | BlackRock / Securitize | ~$2.5 billion |

| OUSG | Ondo Finance | ~$588 million |

| FOBXX/BENJI | Franklin Templeton | ~$959 million |

| USTB | Superstate | ~$621 million |

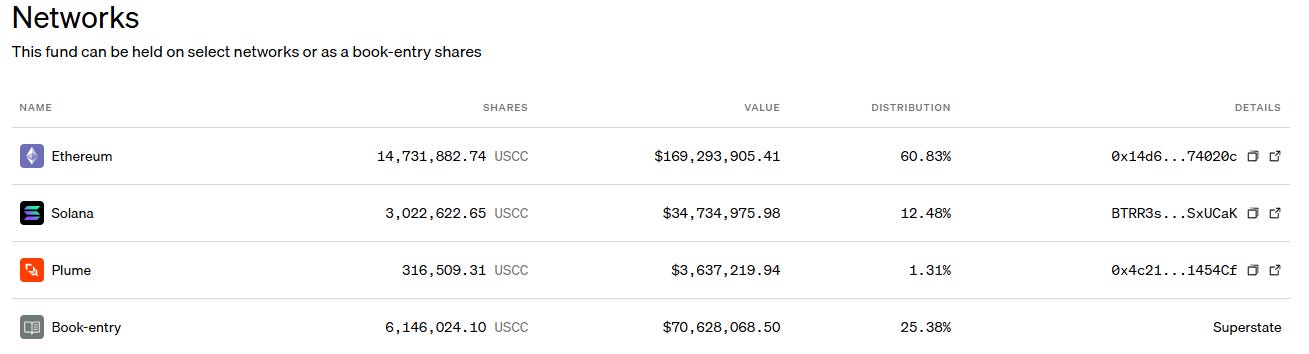

| USCC | Superstate | ~$169 million |

DeFi carry trade

Tokenization opens the door to strategies previously reserved for large institutional players. The core concept is a programmable carry trade – interest rate arbitrage across jurisdictions and protocols.

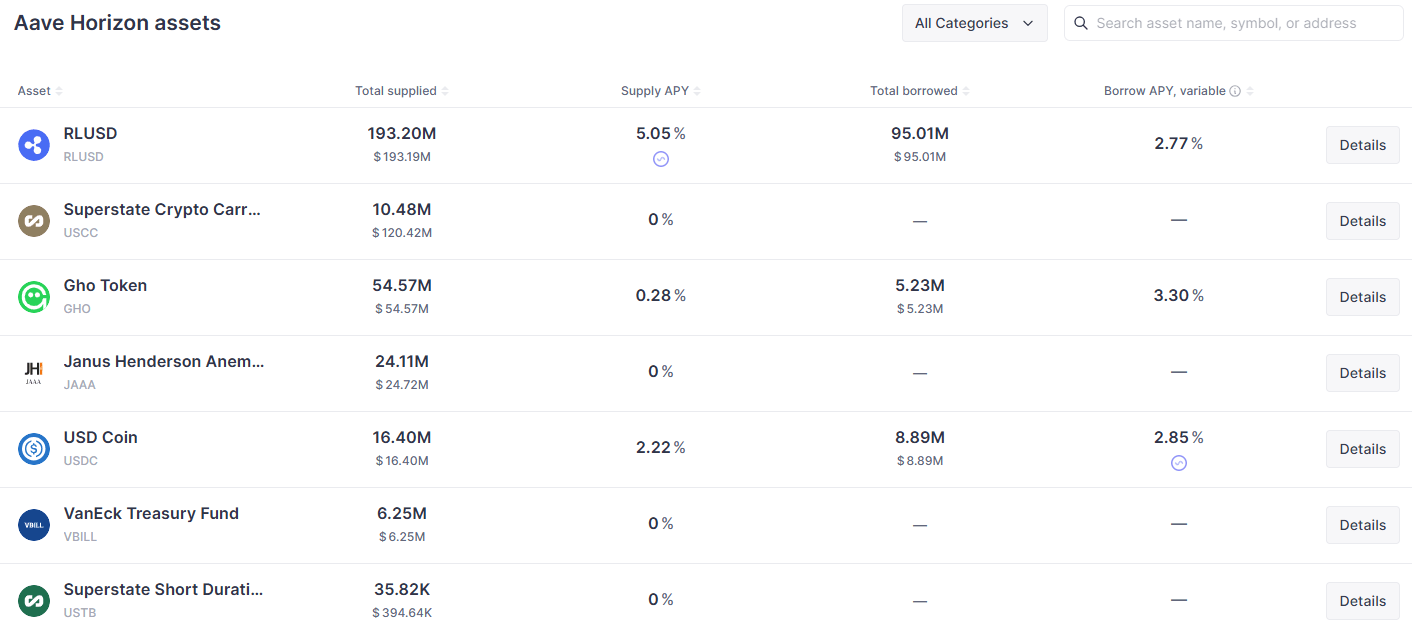

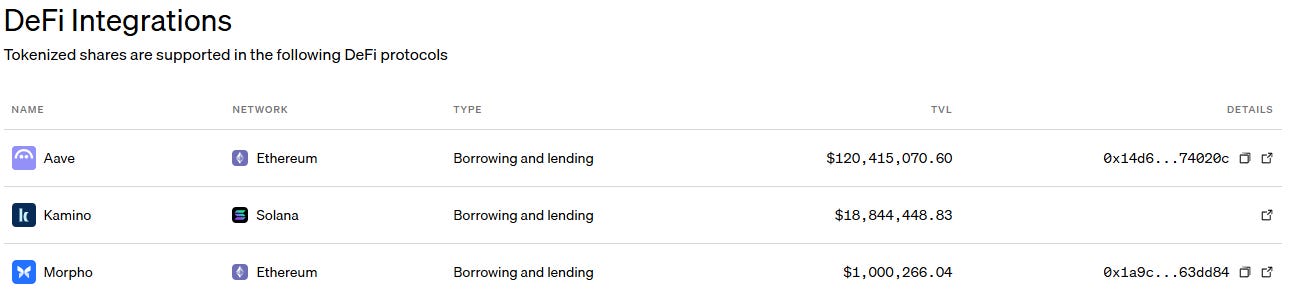

To implement such a strategy, Aave Horizon – a lending market built on Aave Protocol v3.3 and launched in August 2025 – enables investors to post tokenized RWAs (money market funds, Treasuries, index funds) as collateral to borrow stablecoins. The platform has attracted $300 million in deposits and around $100 million in loans, making it the largest RWA‑backed lending market on‑chain.

A hypothetical programmable carry trade with TMMFs would look as follows:

Base yield “anchor”. The investor first builds a core position in a highly stable tokenized money market fund from a developed market – for example, OUSG or USTB.

Collateralization on Aave Horizon. These tokens are supplied as collateral to Aave Horizon: the investor deposits OUSG/USTB, receives a borrowing capacity in stablecoins, and the LTV and liquidation thresholds are set by the protocol’s risk parameters.

Yield enhancement via EM‑TMMFs. Against this collateral the investor borrows stablecoins and converts them into tokens of hypothetical tokenized money market funds from emerging markets (Brazil, South Africa, Russia, India, etc.), where nominal rates are structurally higher. At present, there are virtually no publicly accessible tokenized MMFs in such jurisdictions, so this is a forward‑looking construct contingent on local asset managers and regulators embracing tokenization.

FX risk hedging. EM fund yields are denominated in BRL/ZAR/INR, while both collateral and debt are in USD‑stablecoins. The baseline approach is to lock in FX:

Open short positions in perpetual futures or swaps on the relevant FX pairs/index via Hyperliquid or another institutional‑grade DEX.

Structure the position so that P&L on the derivative offsets changes in the local currency vs. USD.

Dynamically resize the hedge as EM‑fund exposure and margin evolve.

Full programmability. The entire strategy can be wrapped into a smart contract under ERC‑4626 or ERC‑7540: collateral posting, borrowing, EM‑TMMF purchase, hedge initiation and rebalancing, collateral‑health management, and auto‑liquidations. This transforms an institutional‑grade carry trade into a transparent, programmable product accessible at materially lower ticket sizes.

The key point is that, on‑chain today, tokenized funds are predominantly U.S. – and to a lesser extent European – vehicles. MMFs from emerging markets are not yet broadly tokenized, but regulatory trajectories and successful developed‑market precedents suggest a high probability that local managers and exchanges will move toward tokenizing their money funds over the coming years.

Outlook and Prospects

The convergence of traditional and decentralized infrastructure is unfolding along several dimensions at once:

BUIDL as collateral: BlackRock’s tokenized fund is now accepted as collateral on Binance, Crypto.com, and Deribit, evolving from a yield‑bearing token into core market infrastructure.

Ripple Prime + Hyperliquid: In early 2026, institutional prime broker Ripple Prime integrated Hyperliquid, enabling institutional clients to trade on‑chain derivatives within a unified margin framework alongside traditional assets (FX, fixed income, swaps).

SEC S‑1 registration for Hyperliquid: The platform is moving toward regulatory alignment with major jurisdictions.

The tokenized RWA market is at an inflection point, transitioning from pilots to large‑scale deployment. Leading institutions project the following:

| Source | Report date | RWA AUM forecast |

| BCG и Ripple | 7 April 2025 | $18.9 trillion by 2033 |

| Standard Chartered | 27 June 2024 | $30.1 trillion by 2034 |

| McKinsey | 20 June 2024 | $2 trillion by 2030 |

| 21.co | 18 June 2023 | $6.82 trillion by 2030 |

| Citigroup | 30 March 2023 | $4 trillion by 2030 |

Conclusion

Money market instruments are undergoing a transformation comparable to the shift from physical certificates to electronic book‑entry systems. The $18+ trillion repo market – the backbone of global liquidity – is gaining a digital extension through tokenized funds, whose aggregate size has already surpassed $10 billion and continues to grow at double‑digit rates quarter‑on‑quarter. The convergence of institutional infrastructure (BlackRock, VanEck, Franklin Templeton) with decentralized protocols (Aave Horizon, Ondo Finance, Centrifuge) is giving rise to a new class of programmable financial strategies – from automated carry trades to multi‑currency rate arbitrage – strategies that until recently were the preserve of the largest institutional players.

However, every return stream is a reflection of embedded risk. EM currency volatility, interest‑rate dynamics, regulatory uncertainty, and smart‑contract vulnerabilities all demand a rigorous, system‑level approach to risk management. For investors considering such strategies, it is critical not only to understand the mechanics of yield generation but also to maintain strict control over each link in the risk chain.

This material has been prepared for research purposes only and does not constitute investment advice. Investments in RWAs involve risks, including smart‑contract vulnerabilities, regulatory uncertainty, counterparty risk, and market volatility. Conduct your own due diligence before committing capital.

The topic discussed here is just one vector within the broader field at the intersection of institutional finance and decentralized protocols. Subscribe to our channel to receive institutional‑grade analytical content: strategy breakdowns, macroeconomic analysis, reviews of new DeFi and TradFi instruments, and practical guides to portfolio construction.